EVEN AS inter-ministerial consultations for 2022-23 revised estimates of Union finances begin Monday, October 10, internal discussions within the Prime Minister’s Office and the Ministry of Finance seem to suggest that the cascading impact of a worse-than-anticipated global downturn may dent the budget arithmetic in the second half of the current financial year.

So far, the political leadership has been somewhat sanguine with the upsides – an uptick in GDP growth during April-June; steady tax revenues, including monthly Goods and Services Tax (GST) collections averaging around Rs 1.48 lakh crore; and more leeway for the Indian rupee to depreciate on the REER (Real Effective Exchange Rate) basis vis-à-vis other countries.

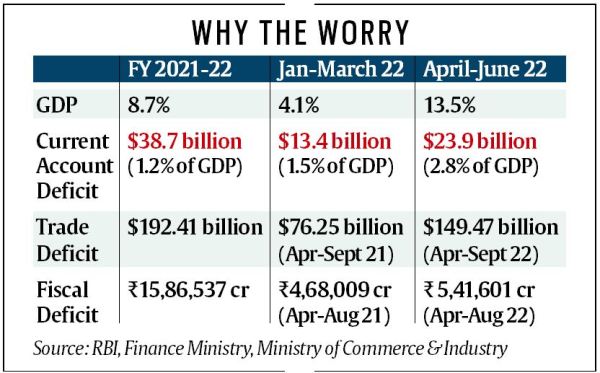

But policy makers are now pointing to multiple headwinds: pressure on the twin deficits (fiscal deficit and the current account deficit), concerns over private investment and job creation, and the continuing distress in the MSME (Micro, Small and Medium Enterprises) sector. All this, together with a hike in policy rates by the RBI – 190 basis points since March – is expected to dampen the nascent consumption-led domestic recovery, even as the fear of a global recession looms large.

While tax revenues have posted robust growth, it is being felt that the revenue trend will have to turn better during October-March, since non-tax revenues are not expected to be substantial. “(In a slowing economy) this will not be easy. We have to think what can be done to manage this. Receipts should increase. If they don’t, we will need to cut expenditure. The other option is to borrow more, but then we would want to maintain a fair degree of predictability. So, the space to manoeuvre shrinks,” an official involved in the discussions said.

The additional spending on account of inflated subsidies bill and any further extension to the free foodgrains scheme is seen as adding to the fiscal burden, which may necessitate reducing government expenditure. Some signs of rationalisation in spending are already visible. While capex growth during April-August jumped 46.81 per cent, the Centre’s non-interest revenue expenditure growth has contracted 3.31 per cent during the same period. “This (contraction) is a bit perplexing as to why the Union government is restraining its budgeted expenditure when there is no shortfall on the tax revenue front,” said Sunil Sinha, Principal Economist, India Ratings.

The Budget had pegged the fiscal deficit at 6.4 per cent of the GDP for 2022-23, which it expects to maintain given the upside in GDP in nominal terms due to high inflation. In the review meetings beginning Monday, it is expected that schemes which have not seen substantial offtake could get discontinued.

Another big worry is on the external front, with fears of further aggressive rate hikes by the Federal Reserve resulting in FII outflows. India’s current account funding needs continue to be large, with the deficit for the current financial year expected to widen to levels last seen in 2013. Higher, expensive imports and flagging exports due to a global slowdown has resulted in higher trade deficit. It has widened to $26.72 billion, with exports shrinking by 3.52 per cent to $32.62 billion in September.

The spill-over effects of the continuing aggressive monetary tightening in the United States, the Chinese slowdown due to a hard Covid-19 policy, and the unpredictability of crude oil prices given a volatile geo-political scenario, have only complicated the management of the external sector. The central bank’s intervention in the currency market to prevent the rupee from depreciating more sharply against the US dollar has already resulted in a sharp dip in the country’s forex reserves.

There is some comfort to be drawn from a further moderation in commodity prices due to demand dissipation in the global economy. Crude remains a lingering worry though and with oil prices remaining on the boil, what is of particular concern to policymakers is the limited wriggle room available to pass on the benefits during short windows of low prices. The consequence being inflation may remain high for longer than expected because fiscal intervention through higher subsidy may not be prudent.

On the growth front, one major concern is that private investment is not showing meaningful signs of revival. Union Finance Minister Nirmala Sitharaman had to recently prod the industry to step up investments during a recent interaction. The government’s bet on crowding in private investments has not yielded much success “despite multiple interventions on the policy side”, a government official said.

Given the complexities, a constant refrain among policymakers these days is that fiscal and monetary policies need to be in consonance. “The signs are not too bright globally. So, one has to keep the armour on. We need to exercise maximum prudence. It is important that fiscal and monetary policies should be backing up each other rather than working at cross purposes,” another official involved in the deliberations said.